Editor's Picks (Total records: loading...)

Tesla Stock Jumps 8% as Free Supercharging for Life Makes a Comeback

Tesla Revives Free Supercharging to Boost Slumping Model S Sales 28 minutes ago

Microsoft's $80 Billion AI Push: A Game-Changer in U.S.-China Tech Battle

Brad Smith Calls for U.S. AI Strategy as Microsoft Invests Record Amount 41 minutes ago

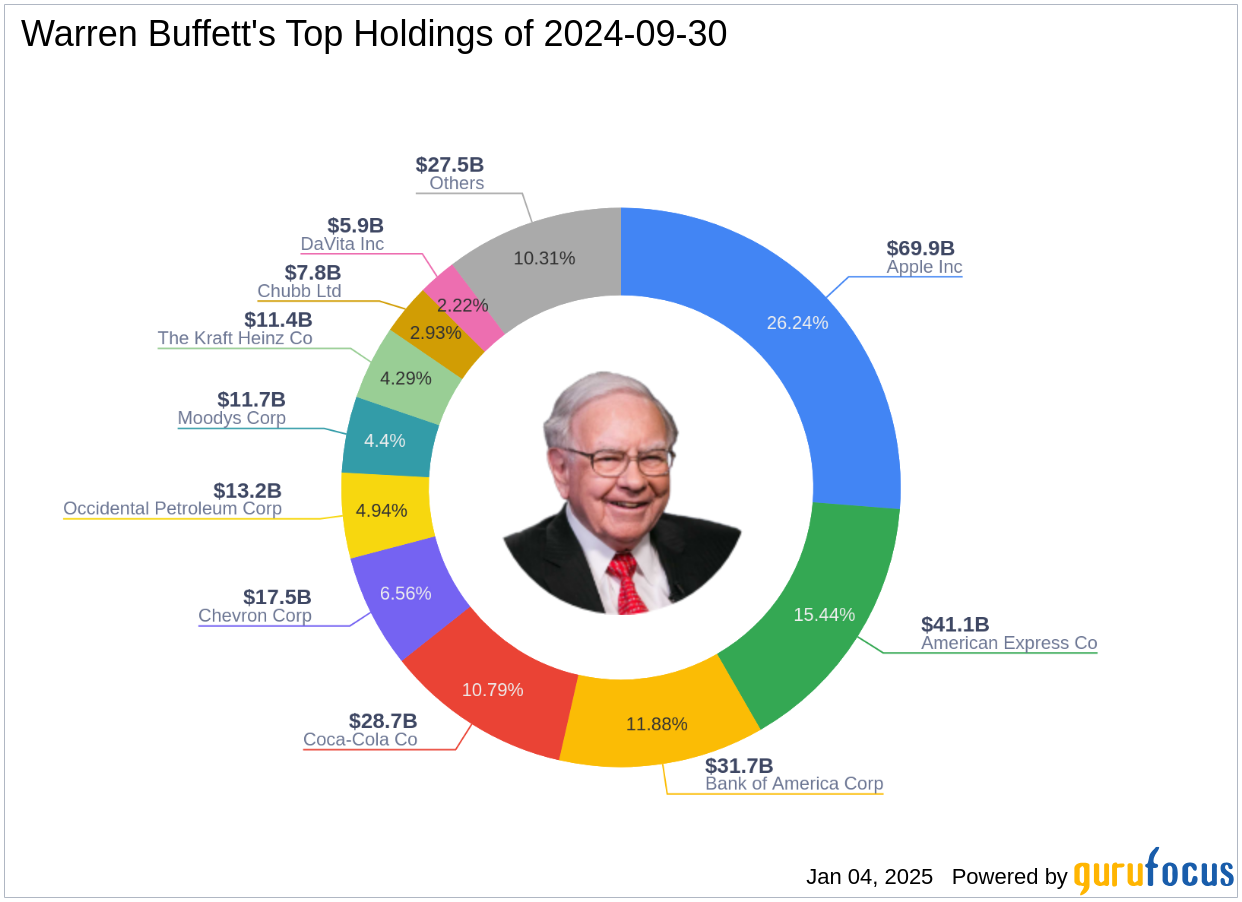

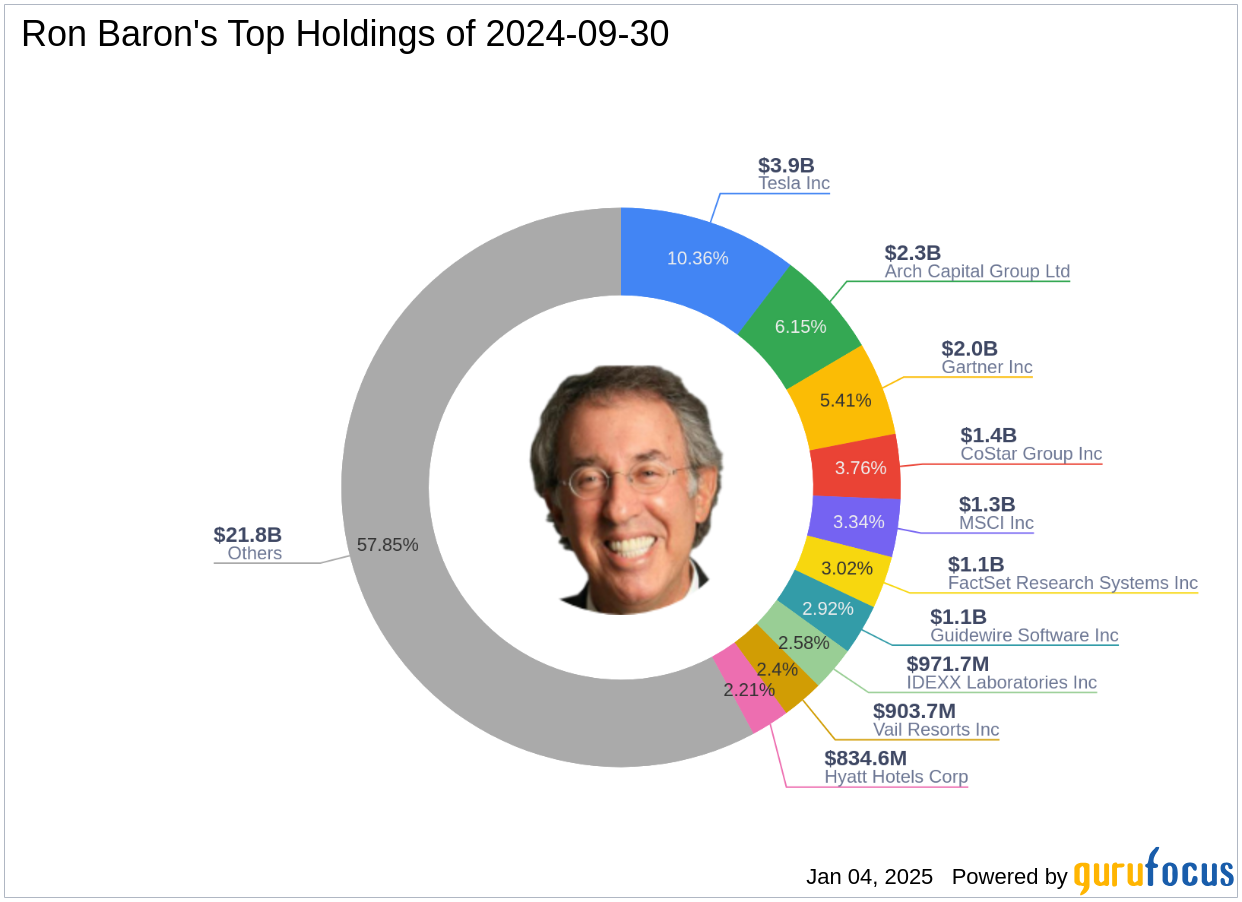

Ron Baron's Strategic Acquisition in Indie Semiconductor Inc

6 hours ago

Market Today: Cerence AI Partners with Nvidia, Wolfe Research's Top Picks for 2025

9 hours ago

Nvidia Leads Tech Surge: Evercore ISI Forecasts 22% S&P 500 Growth in 2025

Evercore ISI projects the S&P 500 to rise 22% in 2025, reaching 7,200. 10 hours ago

Nvidia Tops Semiconductor Ownership Among U.S. Fund Managers: BofA Report

Nvidia's portfolio weighting increased to 1.01x, amid valuation concerns. 10 hours ago

Synaptics Gains on Google Collaboration to Advance Edge AI in IoT Applications

Synaptics partners with Google to enhance Edge AI capabilities for IoT devices. 11 hours ago

Disney's Blockbusters Dominate 2024, Spain Channel Closure Signals Shift

Disney's "Inside Out 2" was 2024's highest-grossing picture and broke new animated movie records. 11 hours ago

Netflix Accidentally Reveals June 2025 Release Date for 'Squid Game' Season 3

The streaming giant quickly removed the video and has not confirmed the release date, stating schedules are unfinalized. 11 hours ago

Nvidia Gains as Bank of America Reaffirms Top Pick Ahead of CES

Bank of America reiterated its "Top Pick" rating with a $190 price target, citing Nvidia's strong positioning ahead of CES. 11 hours ago

Apple Targets Price-Sensitive Shoppers in China With iPhone Discounts Amid Local Rivalry

The promotion also includes savings of up to 800 yuan on MacBooks, available through select payment methods. 11 hours ago

App Store Revenue Lifts Apple's Q1 as Digital Services Demand Soars Globally

Apple's App Store revenue surges 12.7% YoY in December, boosting Q1 growth despite hardware challenges. 12 hours ago

Microsoft's $80B AI Bet: Data Center Expansion Fuels Nvidia and AMD Surge

Microsoft's $80B data center investment underscores AI ambitions, boosting Nvidia and AMD shares 12 hours ago

Nvidia Tops Semiconductor Rankings as Fund Managers Bet Big on AI-Led Growth

Nvidia tops U.S. fund manager holdings as AI and high-performance computing drive long-term semiconductor confidence 12 hours ago

TreeHouse Foods Expands with Harris Tea Acquisition and Reaffirms FY24 Guidance

12 hours ago

Rivian's Stock Surges on Strong Q4 Performance and Future Prospects

12 hours ago

More GuruFocus Links

All-In-One Screener Latest Guru Picks Warren Buffett Portfolio Ben Graham Net-Net Real Time Picks Buffett-Munger ScreenerLatest Comments

Survey

We'd love to learn more about your experiences on GuruFocus.com and how we can improve!

Take Survey

Follow Us

Disclaimers